Chronically Ill: The Insurance Definition Advisors Need

"Chronically ill" has two meanings, and the gap between them matters. In medicine, it describes anyone with a long-term condition that needs ongoing care — diabetes, arthritis, well-managed COPD. In insurance, it has a precise statutory definition under IRC §7702B(c)(2) that determines whether a client's long-term care rider, chronic illness rider, or accelerated death benefit pays out tax-free.

If you sell life insurance with living benefits to New Jersey clients, the second definition is the one that decides whether the policy actually does what they bought it for. This is a refresher worth having clear in your head before the next client review.

The Plain-English Medical Definition

In ordinary medical use, a chronic illness is a health condition that lasts a year or longer and either requires ongoing medical attention or limits activities of daily living. The CDC uses this definition for public-health work, and the major patient-facing sources — Cleveland Clinic, MedlinePlus, Healthline — all land in roughly the same place.

By that standard, a huge slice of the U.S. population qualifies. About 60% of American adults live with at least one chronic condition, and roughly 40% have more than one. High blood pressure, type 2 diabetes, arthritis, asthma, and high cholesterol top the list.

This is also exactly the definition that's too broad to use in an insurance contract. A client with well-controlled hypertension is "chronically ill" in the medical sense. They are not chronically ill in the sense that triggers a long-term care benefit. The carrier needs a brighter line.

What "Chronically Ill" Means in an Insurance Contract

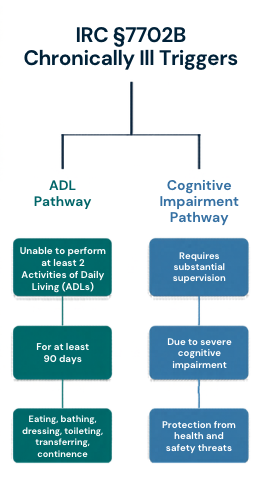

That brighter line lives in Section 7702B of the Internal Revenue Code. Under IRC §7702B(c)(2), a chronically ill individual is someone a licensed health care practitioner has certified as meeting at least one of three conditions:

The §7702B(c)(2) trigger:

The ADL trigger— unable to perform at least two of six activities of daily living without substantial assistance from another person, for a period of at least 90 days, due to loss of functional capacity; OR

The disability-similar trigger— having a level of disability similar to the ADL trigger, as determined under Treasury regulations; OR

The cognitive impairment trigger— requiring substantial supervision to protect against threats to health and safety due to severe cognitive impairment (Alzheimer's, dementia, and similar).

The certification must have been made within the prior 12 months for the trigger to be active.

Three things to flag about this definition that get missed in client conversations:

The 90-day expectation.The "90 days" is an expected duration, not a waiting period the client serves before benefits begin. A practitioner certifies that the impairment is expected to last 90 days or more. Most policies still impose a separate elimination period (typically 0–180 days) before benefits flow.

The 12-month re-certification.The status isn't certified once and forever. The client's certifying practitioner has to renew within the prior 12 months. Clients on long claims sometimes assume the original certification carries indefinitely; it doesn't.

The disability-similar pathway.Most explanations skip clause (ii) — a disability "similar to" the two-ADL standard. This gives carriers and Treasury some latitude that occasionally matters at the edges of a claim. Worth knowing it exists.

The Six Activities of Daily Living (ADLs)

The ADLs are listed in §7702B(c)(2)(B). For a contract to qualify as long-term care insurance under §7702B, it must take at least five of these six into account when determining whether someone meets the ADL trigger.

Eating— feeding oneself by any means, including by feeding tube or IV

Toileting— getting to and from the toilet, getting on and off, performing related personal hygiene

Transferring— moving in and out of a bed, chair, or wheelchair

Bathing— washing oneself in a tub or shower, including getting in and out

Dressing— putting on and taking off necessary clothing and any required braces or artificial limbs

Continence— maintaining control of bowel and bladder function, or performing related personal hygiene if not

The IRS has issued safe-harbor guidance on what counts as "substantial assistance" — bothhands-on assistance(a caregiver physically helping) andstandby assistance(a caregiver within arm's reach, ready to prevent injury) qualify. See IRS Notice 97-31 for the safe-harbor definitions if you need to walk a client through an edge case.

§7702B vs §101(g): Which Code Section Applies to Which Product?

Here's where advisors trip up most often. Both code sections reference the same "chronically ill" definition, but they govern different product categories and have different tax mechanics. If you sell life insurance with living benefits, you need to know which one your contract is filed under before you tell a client how their benefit will be taxed.

IRC §7702BIRC §101(g)GovernsQualified long-term care insurance contracts and LTC ridersAccelerated death benefits, including chronic illness riders on life insurance"Chronically ill" definition§7702B(c)(2) — three triggers aboveCross-references §7702B(c)(2) for the chronic illness triggerTypical productStandalone LTC policy or LTC rider on life/annuityChronic illness rider on a life insurance policy; viatical settlementsPermanency requirementNo requirement that condition be permanentMany §101(g) chronic illness riders require the condition to be reasonably expected to be permanentTax treatment of benefitsExcluded from income, subject to per diem cap if paid on per-diem basisExcluded from income as accelerated death benefitTypical extra premiumExplicit LTC rider premiumOften minimal or built into base policy (death benefit may be discounted instead)Agent CEOften requires LTC-specific continuing educationUsually does not require LTC CE (filed as life insurance)

The practical implication: a client who tells you "I have long-term care coverage on my life policy" may have a §7702B LTC rider or a §101(g) chronic illness rider. Those are not the same product. The §101(g) rider is often cheaper and easier for carriers to file, but it may impose a permanency requirement that excludes recoveries the §7702B rider would have covered. At point of sale, the client should know the difference. At claim, it controls what they get.

[E-E-A-T spot — your specifics go here]:If you've worked a claim where the §7702B vs §101(g) distinction surprised a client, drop in one sentence. Real claim stories from NJ NAIFA members carry weight that general explanations can't. Delete this callout if you'd rather skip it.

What This Means for Your New Jersey Clients

A few NJ-specific notes worth keeping in mind:

The NJ Long-Term Care Partnership Program. New Jersey participates in the federal LTC Partnership Program, which lets clients who exhaust qualifying private LTC coverage protect an equivalent amount of assets when applying for Medicaid. Partnership-qualified policies must meet §7702B requirements plus state-specific consumer protection standards. Worth flagging for clients who view LTC insurance as part of an estate-protection strategy.

The NJ Department of Banking and Insuranceregulates LTC and life insurance products sold in the state, with its own rules on rate increases, replacement, and disclosure. The chronically ill definition is federal; the consumer protections around it can be state-specific. When in doubt, the NJ DOBI is the right starting point for a regulatory question.

The conversation to have during a policy review:

When you pull up a client's life insurance policy and they have a chronic illness or LTC rider, three questions pin down what they actually own:

Is the rider filed under §7702B or §101(g)?

Does it require the condition to be permanent?

What's the elimination period and the benefit amount?

If the client can't answer those questions, neither can their family at claim time. Spending five minutes on this during the annual review is one of the highest-leverage things you can do for their household.

[E-E-A-T spot — your process goes here]:If NAIFA-NJ has a standard policy review checklist or talking points members use with clients, mention it here. Specific process beats generic advice.

When the conversation moves into estate planning or Medicaid eligibility — particularly with the Partnership program — the right move is to bring in an elder law attorney. That's their lane, not yours, and saying so explicitly builds trust with the client.

Frequently Asked Questions

What does "chronically ill" mean in life insurance?

Under IRC §7702B(c)(2), a chronically ill individual is someone certified by a licensed health care practitioner as either unable to perform at least two of six activities of daily living for at least 90 days, or requiring substantial supervision due to severe cognitive impairment. The certification must be renewed within the previous 12 months. This is the trigger that activates LTC riders and chronic illness riders.

Is "chronically ill" the same as "terminally ill" for insurance purposes?

No. Terminally ill is defined separately, generally as a condition reasonably expected to result in death within 24 months under §101(g)(4). Both definitions can trigger an accelerated death benefit, but they have different certification standards and may have different tax treatment.

Are payments to a chronically ill insured tax-free?

Generally yes, when the contract qualifies under §7702B or §101(g) and the insured is properly certified. Per-diem payments are subject to a cap (adjusted annually by the IRS); reimbursement-basis payments are not. The carrier reports payments on Form 1099-LTC; clients should expect to receive one.

What conditions count as "chronically ill" for insurance?

The trigger is functional, not diagnostic. There's no list of qualifying diagnoses. What matters is whether the insured can perform daily activities without substantial assistance, or whether they require substantial supervision due to cognitive impairment. A client with advanced Parkinson's, late-stage Alzheimer's, or significant disability following a stroke could meet the trigger. A client with well-controlled diabetes would not.

Do all life insurance chronic illness riders work the same way?

No. Riders filed under §7702B and riders filed under §101(g) reference the same "chronically ill" definition but differ in product structure, tax mechanics, and often in whether the condition must be expected to be permanent. Read the rider language before quoting the benefit.

Explore NAIFA Benefits

The chronically ill definition is one of those topics that sits quietly in a contract until a claim activates it — and then everything depends on the advisor having explained it correctly at point of sale. NAIFA-NJ exists to keep advisors sharp on exactly these kinds of details, through CE, chapter events, and the resources our members rely on.

Want to grow your practice with the support of a national network? Explore NAIFA benefits.